In 2023, the global economy struggled to recover, and many industries faced growth pressure. However, the new energy sector broke through the trend and maintained a steady growth momentum. The green transformation of the energy structure has accelerated, and various new energy application scenarios have been continuously implemented, creating a broad space for the upstream core component market.

Among them, the rapid expansion of the three major fields of new energy vehicles, photovoltaic, and energy storage has directly driven the demand for magnetic components. These three fields have extremely high requirements for the stability of energy conversion and signal transmission, and magnetic components, as core supporting parts, directly affect the operation effect of the entire system.

Among the many magnetic components, amorphous alloy cores and nanocrystalline cores, with their unique performance advantages, have become increasingly widely used in the field of new energy vehicles. This article focuses on analyzing the application value, market opportunities, industry development trends, and enterprise layout directions of these two types of cores in new energy vehicles.

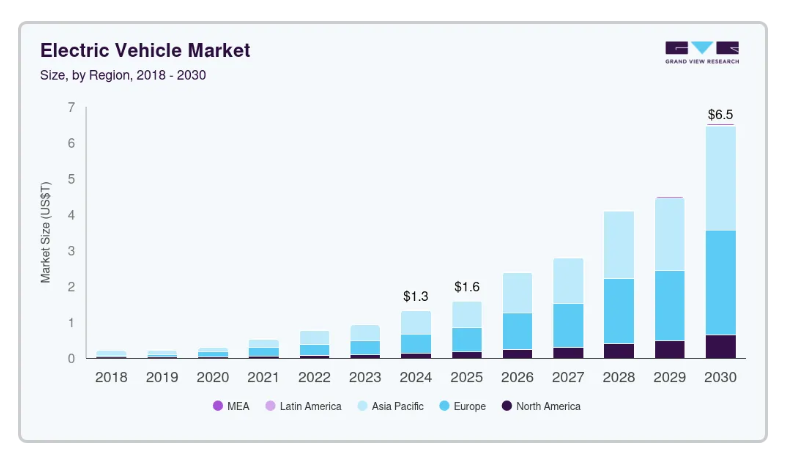

In 2023, the global new energy vehicle (NEV) market continued to expand; production and sales volumes reached approximately 15 million and 13.5 million units, respectively. With its market penetration rate steadily rising, the sector has emerged as the core driving force behind the transformation of the global automotive industry. As the central hub of the global NEV market, China accounted for approximately 65% of global sales, maintaining its position as the global market leader for several consecutive years.

The European market also delivered impressive results. Although the EU adjusted its 2035 ban on internal combustion engines—relaxing the carbon emission reduction target for new cars from 100% to 90%—it did not ease its overall emission reduction requirements. Instead, through supportive policies such as subsidizing small electric vehicles and promoting the electrification of corporate fleets, the region continued to drive growth in NEV sales.

Industry forecasts indicate that by 2025, global NEV production and sales volumes will climb further to 20.3 million and 19.3 million units, respectively, demonstrating that the market still possesses vast room for growth. As a major powerhouse in both the production and consumption of NEVs, China will continue to play a leading role, while the growth potential of overseas markets is also expected to be gradually unleashed.

The NEV industry chain encompasses multiple stages—including R&D, manufacturing, component supply, and retail sales—characterized by its extensive scope and broad range of involved sectors. Within this chain, the core vehicle systems primarily fall into three categories: infotainment systems, autonomous driving and body control systems, and electrification systems.

Infotainment systems are primarily responsible for in-cabin audio-visual functions, navigation, and similar features; consequently, their demand for magnetic components is relatively limited. Autonomous driving and body control systems focus on vehicle safety and handling; while they do utilize certain magnetic components, the quantities involved are modest, and the performance requirements for these components are relatively standard.

Electrification systems constitute the core of any NEV, covering critical aspects such as battery management, electric propulsion, and charging infrastructure. This category also represents the system with the highest reliance on magnetic components. Whether for energy conversion or signal transmission, these systems depend heavily on the support provided by various types of magnetic cores, thereby establishing magnetic components as indispensable core parts within the electrification architecture.

The electric propulsion system serves as the "heart" of a new energy vehicle, responsible for converting the electrical energy stored in the battery into mechanical energy to drive the vehicle forward. Within this process, motor control and power conversion represent the critical stages—areas where the demand for magnetic cores is particularly pronounced. Motor control requires a stable magnetic field to achieve precise speed regulation and ensure smooth vehicle operation; power conversion, conversely, relies on magnetic cores to facilitate efficient energy transfer and minimize energy loss. Whether in purely electric vehicles or hybrid models, the performance of the electric drive system is inextricably linked to the quality and selection of its magnetic cores.

On-Board Chargers (OBCs) and DC-DC converters are critical components for the charging and power supply systems of new energy vehicles, serving as primary application scenarios for amorphous alloy and nanocrystalline magnetic cores. These devices operate in complex environments and are subject to rigorous requirements regarding power output, efficiency, and stability.

The On-Board Charger is responsible for converting household AC power into DC power suitable for charging the vehicle's battery. Currently, OBCs with power ratings of 3.3 kW and 6.6 kW are standard in the passenger vehicle market, while the commercial bus sector utilizes high-power units ranging from 40 kW to 80 kW. Every vehicle is equipped with at least one OBC, and certain models may incorporate additional units depending on specific requirements.

DC-DC converters, on the other hand, are responsible for stepping down the battery's high-voltage power to a lower voltage level, thereby powering low-voltage onboard systems such as interior lighting, central control units, and sensors; vehicles are typically equipped with multiple DC-DC converters. Given the substantial power demands and the high volume of these devices, the market demand for amorphous alloy and nanocrystalline magnetic cores remains exceptionally strong.

As a significant segment of the new energy vehicle market, hybrid electric vehicles present unique requirements for magnetic components—among which the boost inductor plays a particularly critical role. Boost inductors are primarily utilized within the boost converters of hybrid drive systems to step up the battery's low voltage to the high voltage required by the electric motor, thereby reducing current levels and minimizing device losses.

This design approach allows for a reduction in the number of individual battery cells, thereby lowering battery costs, while simultaneously enabling system miniaturization without compromising power output. In terms of the cost breakdown per vehicle, the total value of magnetic components is estimated to range between $149 and $179; within this total, amorphous alloy and nanocrystalline magnetic cores—distinguished by their superior performance—account for a substantial proportion of the cost.

The primary reason amorphous alloy and nanocrystalline cores have become the preferred choice for new energy vehicles (NEVs) lies in their ability to precisely address the core requirements of these vehicles. Compared to traditional magnetic cores, their advantages are far more pronounced—advantages that directly resolve critical pain points encountered in practical applications.

High efficiency and low loss constitute one of their core advantages. Within electric drive systems and charging modules, energy conversion inevitably entails some degree of loss; however, these two types of cores effectively minimize such losses. This results in higher electrical energy utilization efficiency, thereby indirectly enhancing the vehicle's overall energy consumption performance—a perfect alignment with the core NEV imperative of energy conservation and loss reduction.

Interior space in NEVs is extremely limited—particularly given that battery packs already occupy a significant volume—imposing strict requirements on the size and weight of individual components. These amorphous alloy and nanocrystalline cores feature a compact footprint and high power density; they not only satisfy the power requirements of the equipment but also conserve installation space while simultaneously reducing the vehicle's overall weight. This aligns perfectly with the NEV industry's strategic imperative for lightweight design.

Automotive electronic systems are inherently complex; when various devices operate simultaneously, they are prone to generating electromagnetic interference (EMI), which can compromise system stability and even jeopardize driving safety. Amorphous alloy and nanocrystalline cores enhance electromagnetic compatibility (EMC) by suppressing the propagation of common-mode interference. Acting as a "protective shield" for the electronic system, they ensure the stable and reliable operation of all electronic devices.

Beyond new energy vehicles, these two types of magnetic cores also find application in other new energy sectors, such as energy storage systems and charging piles. As the markets for photovoltaics, industrial energy storage, and charging infrastructure continue their rapid expansion, the application scenarios for these cores are constantly diversifying. This expansion broadens their market scope and creates a wealth of new growth opportunities for enterprises within the industry.

Policy guidance at the national level provides a robust foundation for the long-term growth of the magnetic components market within the new energy vehicle sector. Initiatives such as the "Digital China" strategy, the pursuit of carbon neutrality goals, and the Rural Revitalization Strategy are all indirectly driving the development of the new energy industry, thereby stimulating increased demand for magnetic components.

Among these initiatives, the carbon neutrality goal serves as the primary driving force. The nation has explicitly committed to reducing carbon emissions, and sectors such as new energy vehicles, photovoltaics, industrial energy storage, and charging infrastructure represent the key strategic fronts for achieving this objective. The government is providing not only policy support but also continuous improvements to infrastructure—for instance, by establishing the world's largest charging infrastructure network—thereby safeguarding and facilitating the industry's continued growth.

For enterprises, the present moment represents the optimal time to strategically position themselves within the amorphous alloy and nanocrystalline core markets. As the new energy vehicle (NEV) market continues its expansion, demand for these two types of magnetic cores is set to climb steadily. By investing in R&D and production ahead of the curve, companies can seize market initiative and cultivate core competitive strengths.

Concurrently, enterprises must extend their reach across the upstream and downstream industrial chain—encompassing stages such as core manufacturing, wire supply, and production equipment fabrication. A comprehensive industrial chain layout not only helps reduce production costs and mitigates the risk of being constrained by upstream raw material suppliers or downstream market fluctuations, but also enhances product quality and delivery efficiency, thereby enabling companies to better meet customer demands.

Market forecasts indicate that the global NEV market will maintain a trajectory of continuous growth, accompanied by a steady rise in the demand for magnetic components. As core products within this ecosystem, the market size for amorphous alloy and nanocrystalline cores is expected to expand in tandem, signaling broad and promising prospects for the industry.

Key markets are primarily concentrated in three areas: Mid-to-high-end electric vehicles—which impose stringent performance requirements on magnetic cores—serve as the primary application scenario for these two core types; Hybrid vehicles—where market scope has broadened following policy adjustments in regions such as the EU—are driving increased demand for magnetic cores; and Overseas markets—particularly in regions like Europe and Southeast Asia—where rapidly emerging NEV sectors present domestic core manufacturers with extensive export opportunities.

Amorphous alloy cores and nanocrystalline alloy cores are key components in the core links of new energy vehicle electric drive and charging, and their market value continues to rise with the development of the new energy industry. Relevant enterprises need to seize the opportunity, accelerate the research and development, production and upstream and downstream layout of these two types of cores, and at the same time expand the market by relying on fields such as industrial energy storage and charging piles, in order to stand firm in the competition and achieve sustainable development.